Should Washington Own Spirit Airlines?

Exploring whether a state-owned Spirit Airlines could act as a price ceiling for the "Big Four".

For decades, the American sky has been the ultimate laboratory for free-market capitalism. Since the Airline Deregulation Act of 1978, the industry has shifted from a cozy, government-protected club to a hyper-competitive arena where fares plummeted and ‘flying style’ transformed from a luxury experience to a bus-like utility. But as Spirit Airlines (SAVE) faces a liquidity crunch and the collapse of its merger with JetBlue, a once-unthinkable question is being whispered in Washington: Should the government take the stick?

The Shadow of 1978

Before 1978, the Civil Aeronautics Board (CAB) acted as a central planner, dictating routes and standardizing fares. Competition was based on steak dinners and legroom, not price. The Deregulation Act dismantled this, leading to the birth of the LCC (Low-Cost Carrier) model. Spirit Airlines became the poster child for this era, stripping away every amenity to offer the ‘Bare Fare.’ However, the recent volatility of the industry—marked by mass cancellations, pilot shortages, and the erosion of the middle-tier market—has led some to argue that the 1978 experiment has reached a point of diminishing returns.

The Case for Nationalization

Proponents of a government-owned Spirit argue that air travel is an essential infrastructure, no different from the interstate highway system or Amtrak. By nationalizing a carrier like Spirit, the government could:

Ensure Connectivity: Maintaining routes to underserved rural markets that are currently unprofitable for private carriers.

Price Stability: Using a public option to act as a ‘price ceiling’ for the Big Four (Delta, United, American, Southwest).

Employment Security: Protecting thousands of jobs and maintaining a pipeline for pilot training in the interest of national security.

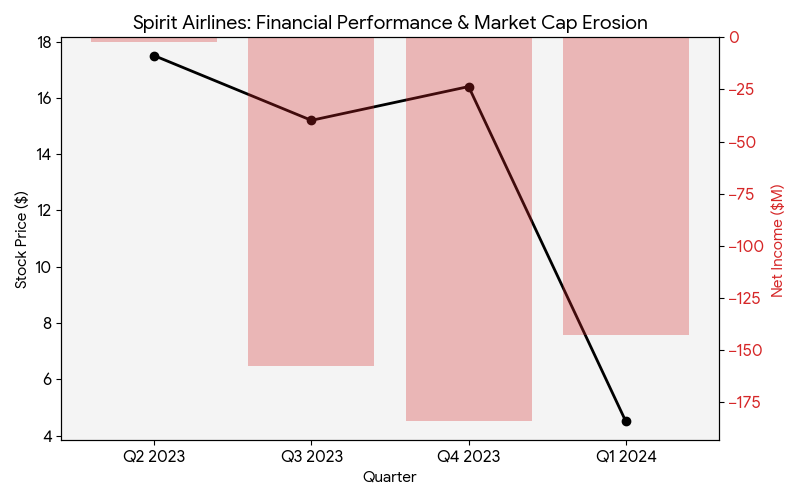

The Financial Reality

The financial data paints a grim picture for Spirit as an independent entity. The chart below illustrates the divergence between market sentiment and operational reality over the past four quarters.

Spirit’s net losses have widened, reaching a staggering $183.7 million in Q4 2023. Meanwhile, its stock price has cratered from the mid-teens to under $5 following the federal block of its merger, signaling a lack of investor confidence in its standalone survival.

The Risks of the “Public Option” in the Sky

Opponents argue that a government-owned airline would be a disaster for efficiency. Critics point to bloated state-owned carriers in Europe and Asia that frequently require multi-billion dollar bailouts. Without the ‘creative destruction’ of the free market, a nationalized Spirit might become a zombie airline—insulated from competition, slow to innovate, and a perpetual drain on the taxpayer.

Furthermore, the 1978 Act was intended to remove politics from the cockpit. A government carrier would likely face political pressure to keep inefficient routes open or hire based on political mandates rather than operational necessity.

Nationalizing Spirit Airlines would be the most significant reversal of U.S. aviation policy in half a century. While it offers a tempting solution to preserve competition and service, it risks creating a bureaucratic behemoth in an industry that moves at the speed of sound. As Spirit’s runway shortens, Washington must decide if it is ready to become an operator, rather than just a regulator.