Evaluating the Soho House Exit Value

How a $50 million personal check kept the lights on at Greek Street.

The high-stakes effort to take Soho House & Co. private has hit a significant financial snag. MCR Hotels, the third-largest hotel owner-operator in the United States, has reportedly informed stakeholders that it is unable to fulfill its $200 million equity commitment, throwing the future of the $2.7 billion merger into uncertainty.

The Vision: A Private Retreat

In August 2025, MCR Hotels, led by CEO Tyler Morse, announced a deal to partner with Yucaipa Companies (controlled by billionaire Ron Burkle) to take the iconic membership club private. The deal was designed to rescue Soho House from the volatility of the public markets, where it has struggled to maintain its “cool factor” while meeting the quarterly growth demands of Wall Street.

Under the original terms:

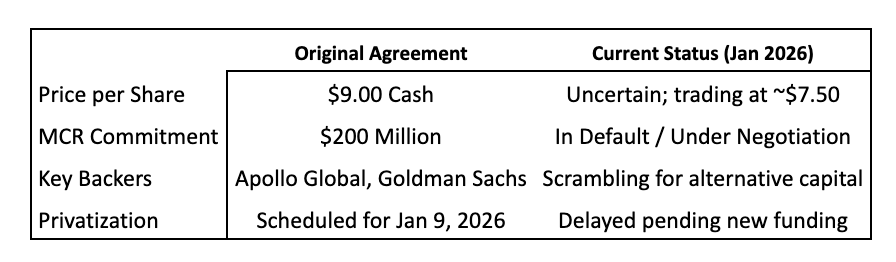

Offer Price: $9.00 per share (an 83% premium over late 2024 prices).

Total Enterprise Value: Approximately $2.7 billion.

The MCR Piece: A $200 million equity injection intended to fund the payout to minority shareholders.

The $200 Million Stumble

The deal reached a crisis point on January 5, 2026, when MCR officially notified Yucaipa that it would not be able to fund its $200 million closing commitment in full. This disclosure, made public via SEC filings, sent Soho House (SHCO) shares into a tailspin, with the stock dropping nearly 20% in a single trading session.

While the exact reasons for MCR’s funding shortfall remain speculative, analysts point to several potential factors:

Tightening Credit Markets: Despite MCR’s massive portfolio, securing liquid equity for a $200 million single-asset commitment has proven difficult in the current rate environment.

Due Diligence Friction: Unconfirmed reports suggest the two parties may have disagreed on the final valuation of Soho House’s international expansion pipeline.

Governance Tensions: The deal would have seen Tyler Morse become Vice Chairman of the board, a move that some insiders suggest may have led to “clashing visions” with existing leadership.

Deal Status at a Glance

Let’s breakdown the deal in question

“Scrambling for Alternatives”

Despite the funding gap, Soho House proceeded with its special stockholder meeting on January 9, 2026, where shareholders overwhelmingly voted to adopt the merger agreement. This puts the company in a “wait and see” posture.

“Yucaipa and the Special Committee are actively engaging with affiliates of MCR and other parties to secure the funding... there can be no assurance that such efforts will be successful.”

— Soho House & Co. SEC Form 8-K Filing

If MCR cannot produce the funds, the deal may require a “white knight” investor or a restructuring of the buyout price. Major players like Apollo Global Management, who were already providing debt for the deal, are reportedly in talks to bridge the gap, though such a move would likely come with steep costs for Soho House’s leadership.

The Eleventh-Hour Wire

Just as the industry began to draft the deal’s obituary, a reprieve arrived with the quiet, kinetic energy of a wire transfer. In a maneuver that feels more like a cinematic rescue than a standard restructuring, Morse Ventures—a private entity controlled by Tyler Morse himself—stepped in to patch the hull. By committing $50 million in personal equity and persuading MCR to provide an additional $50 million, Morse effectively halved the original deficit. The remaining shortfall was absorbed by the heavyweights: Apollo Global and Goldman Sachs upsized their debt facilities to $220 million, while minority shareholders, including the London restaurant titan Richard Caring, agreed to roll over more of their stakes rather than cash out. It was a high-wire act of financial engineering that transformed a public default into a private triumph, proving that while the “mood” of a club is fickle, the machinery of a determined hotelier can still turn a “no” into a “not yet.”

The Dilution of the Sanctuary

The crisis at Soho House is not merely one of balance sheets, but of “vibe” longevity—a far more precarious currency. For years, the club’s primary product was a curated exclusion, a promise that upon crossing the threshold, one would find a sanctuary populated exclusively by the “creative soul.” But in its aggressive sprint toward global scale, that sanctuary has begun to feel more like a departure lounge for the professionalized “influencer” class. The rooms that once buzzed with the messy energy of playwrights and painters are now often silent, illuminated by the uniform glow of MacBooks as members perform the “creative life” rather than living it. In the eyes of its original apostles, the House has committed the ultimate sin of luxury: it became accessible enough to be common, replacing the authentic friction of the bohemian underground with the sterile, predictable hum of a high-end co-working space.